GST/HST Rebates for Non-Profit Housing Providers

10/25/20254 min read

This article is provided for general information only and does not constitute tax or legal advice. Organizations should consult their professional advisors regarding their specific circumstances.

Description of Programs

The CRA has two programs that aim to provide tax relief for developments of rental properties. The CRA also has a default mechanism for refunding HST expenses associated with commercial expenses and a program for tax relief on other general non-profit expenses.

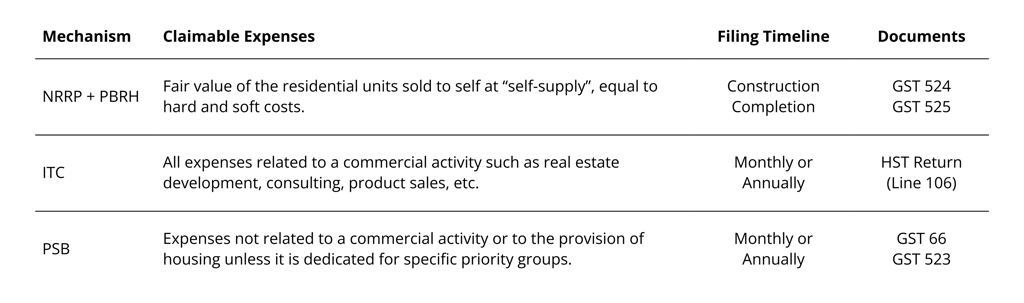

The New Residential Rental Property rebate (NRRP) is a permanent program that allows you to claim back HST upon the completion of a development for “self-supply”, the process of effectively selling a property to oneself, which is intended to make up for the lack of HST payable on rent. This rebate is equivalently a rebate applicable to a property sold to a non-builder owner and later rented out. Without the PBRH top-up, this generally provides a rebate of 36% of the Federal portion of HST up to $6,300 per unit for units valued at less than $350,000, and 75% of the Provincial portion of HST up to $24,000 per unit regardless of their value.

As an extension of the NRRP program, the Purpose-Built Rental Housing rebate (PBRH) provides an additional rebate at self-supply, applicable to all properties starting construction before 2031 and with substantial completion before 2036. It adjusts self-supply rebates to 100% of HST with no maximum limit, provided it is a purpose-built rental with more than four units and not a renovation, although conversions from non-residential properties to residential units are eligible.

In the generation of taxable supplies, the course of a “commercial activity”, you are by default eligible for Input Tax Credits (ITCs) that essentially offset the HST you collect on your sale of products and services with the HST that you pay for inputs to your business, effectively establishing the structure of the Value-Added Tax. Real estate developments are considered commercial activity due to the self-supply rules surrounding them, making them eligible for ITCs. Commercial activities also include consulting services, but do not include lease of rental units as HST is not applied to them. This is a 100% return applied on expenses related to the commercial activities for organizations registered for GST/HST, which may take the form of a cash refund if the claimable ITCs are greater than the HST collected through said commercial activities.

Finally, the Public Service Bodies’ rebate (PSB) offers cash rebates for expenses that are incurred by organizations operating not for-profit and associated with certain activities that are not “commercial” in nature. Unfortunately, only organizations that derive 40% or more of their revenue from government funding or are registered as charitable organizations, however you can be considered to have generated this revenue once you have secured a contract for government funding, even if not having received it in cash.

Commercial Expense ITC Application

Filing a claim for ITCs is done through regular HST return reporting (without any attachments or additional documents), indicating the total amount of HST incurred on eligible expenses on Line 106 of the return. You must, however, also retain supplementary supporting documentation for the HST incurred, such as invoices, receipts, or contracts, which include the following pieces of information:

Supplier’s Business or Trading Name

Invoice Date or Date HST is Payable

Total Amount Payable

Amount of HST Payable or Note that Total Includes HST

Indication of Status of Each Supply for Invoices with Exempt and Taxable Supplies

Supplier HST Registration Number

For expenses that are $500 or more, the documentation must also include:

Buyer’s Name or Trading Name

Description of the Property or Services

Terms of Payment

A registrant claiming ITCs is not required to submit supporting documentation with a GST/HST return. However, the documents must be maintained and retained until the expiration of six years after the end of the latest year to which they relate.

You can claim ITCs for up to four years after the reporting period in which the corresponding expenses were incurred.

Non-Commercial Expense PSB Rebate Application

As with ITCs, filing claims for PSB rebates are done regularly alongside HST returns, however included as a part of a separate form (GST 66). As a qualifying non-profit, you can have 50% of the Federal portion of HST rebated and 82% of the Provincial portion of HST rebated, roughly equalling 69% of HST.

To qualify, an NPO must file a GST 523 for each Fiscal year, at the end of the year, detailing the nature of funding received through government programs, directly and indirectly. While GST 66 forms for PSB rebates should be filed every reporting period for which they are to be claimed, they will not be processed until the end of the Fiscal year, when a GST 523 is completed. As such, you will not receive the cash rebate until the end of the year.

You can claim PSB Rebates for up to four years after the reporting period in which the corresponding expenses were incurred.

There are various exceptions to what expenses organizations can claim rebates on. In addition to purchase of properties (as would be covered under NRRP) and expenses associated with commercial activities (which are covered by ITCs), rebates cannot be claimed on:

Purchases to provide long-term residential accommodation, unless more than 10% of the accommodation is restricted to seniors, youths, students, individuals with disabilities, or individuals with limited financial resources who qualify for occupancy or reduced rents under a means or income test

Purchases associated with a revenue activity that is a taxable benefit to them for income tax purposes, and for which you do not have to collect HST

Purchases associated with a joint venture activity if any of the other co-venturers are not eligible for PSB rebates